Stablecoins processed $33 trillion in 2025. More than two years earlier, Maersk’s TradeLens - one of the most well-funded supply chain blockchain projects ever built - had already been shut down and buried. Both blockchain projects, but one category keeps scaling while the other keeps dying. How did we end up here?

After years of watching enterprise pilots get quietly shelved while DeFi and stablecoins kept growing, I think, among other things, it comes down to an architectural question that most people in the space aren’t asking.

Is blockchain a database, or is it verification layer on top of one?

Two modes of deployment Link to heading

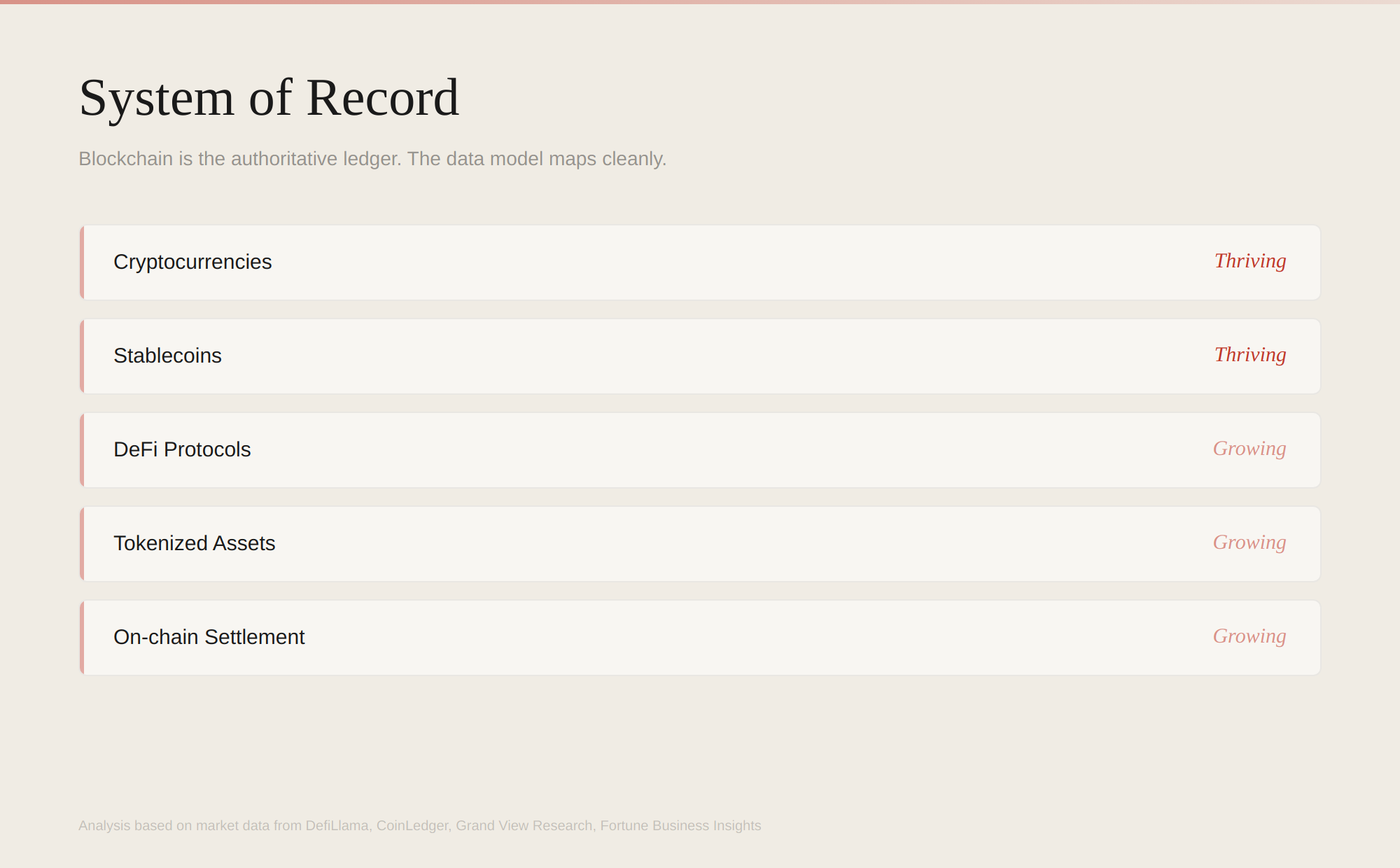

With Bitcoin, nobody has to worry about integrating it with SAP. Accounts, balances, who owns what - the chain holds all of it, with no sync against an external system and no reconciliation with some other “real” database. That self-contained design is what makes it work.

Stablecoins follow the same pattern. So do DeFi protocols, tokenized treasuries, and on-chain settlement systems. Your USDC balance on Ethereum isn’t a copy of a bank database entry. It is the balance. When Aave holds a lending position, that’s not mirrored from somewhere else. Chain state is the position. Period.

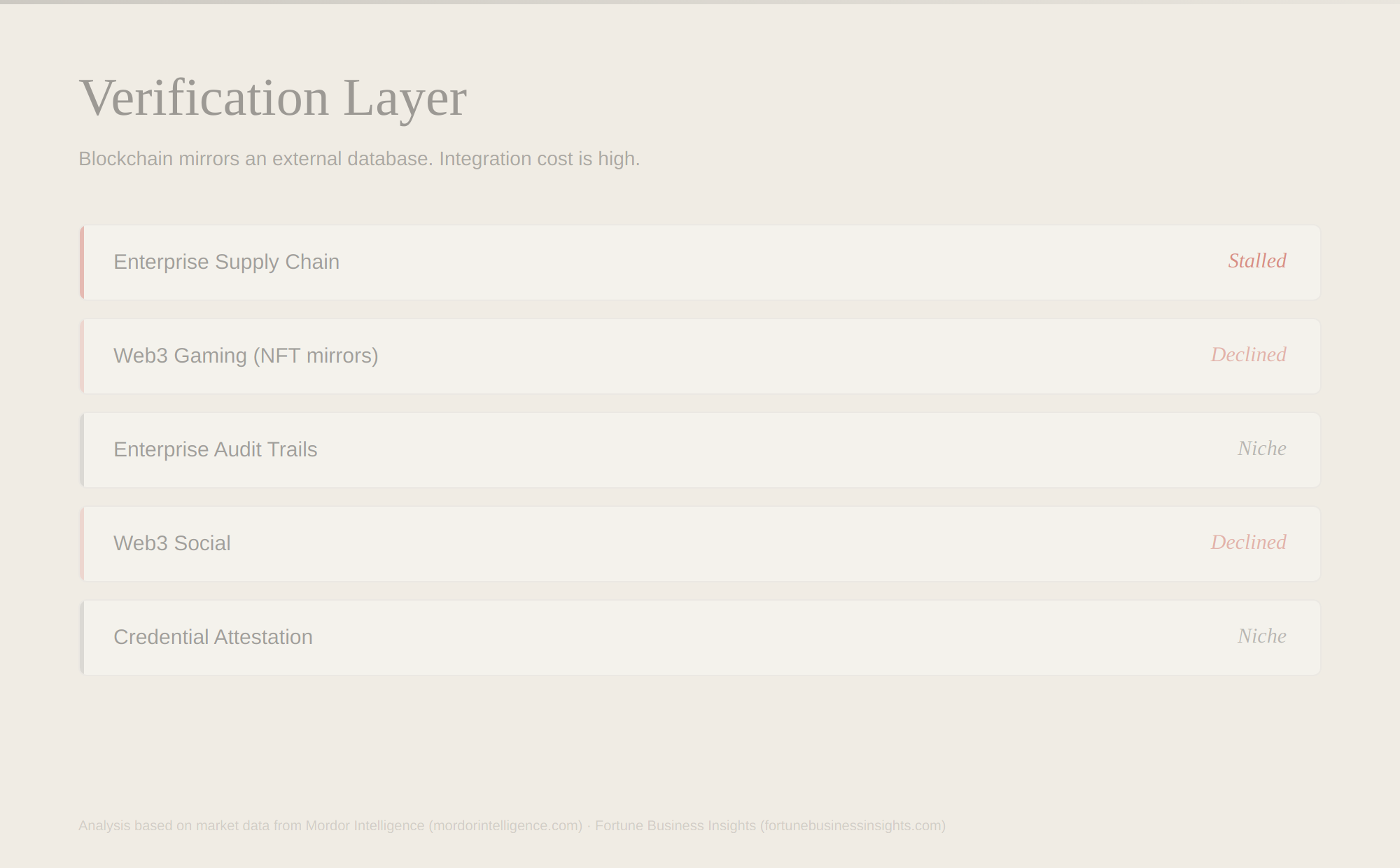

Now compare that to how blockchain got deployed in other use cases. A supply chain company running ERP adds a blockchain layer for provenance stamps. A game studio stores items in their backend database and mints NFTs as events. A bank builds a permissioned chain for audit trails that duplicate records already living in their core banking system.

In all of these, ERP is still the source of truth, or the game backend is, or the core banking platform is - and blockchain is doing add-on work.

That’s where it splits. And it decides pretty much everything that follows about cost, operational burden, and whether a business case ever makes sense.

Blockchain as Verification Layer Link to heading

Layering blockchain on top of existing infrastructure sounds reasonable on a whiteboard. In practice, it means running two systems where you had one, and the integration bill gets ugly fast. You need custodial wallet infrastructure. Key management wired into employee identity systems. Integration logic between enterprise data schemas and whatever format the chain expects. Token procurement for gas fees, plus internal accounting for those tokens. Monitoring to catch failed on-chain transactions. And every partner organization in the workflow has to set up that same stack.

I’ve seen enterprise teams spend months on the key management piece alone. Gas fee accounting creates compliance headaches nobody budgeted for. When a pilot works across two partners, scaling it to twelve means twelve separate integration efforts, each with its own IT team, legal review, and procurement cycle.

Most companies that went through this came to the same conclusion. What blockchain-based verification delivered was not worth what it cost to run. Tech worked fine. ROI didn’t.

One nuance worth flagging here - not every verification layer use case fails. Timestamping a document hash on Bitcoin costs almost nothing and requires zero organizational change. Credential attestation projects that anchor a proof to a public chain without touching enterprise workflows - those can work fine at small scale. Where the money got burned was in the middle zone. Companies trying to run meaningful multi-party business processes through blockchain without making it the authoritative system. Full enterprise deployments with permissioned networks, cross-party consensus, schema translation across dozens of counterparties. That’s where most of the dead pilots lived.

Blockchain as System of Record Link to heading

On-chain data model for financial systems: accounts, balances, ownership, transfers. Traditional finance data model: accounts, balances, ownership, transfers. A 1:1 match at the settlement layer. Integration becomes almost simple compared to enterprise use cases where you’re mapping nested schemas into Merkle trees.

Yes, finance is complex. Derivatives, structured products, KYC/AML pipelines, cross-jurisdictional tax logic. But blockchain doesn’t touch any of that. It sits at settlement and nothing else, where state transitions are atomic and data is flat. “Account A sends X to Account B.” Everything complicated stays in traditional infrastructure that was purpose-built for it.

Here’s a question I keep getting: why can’t other use cases follow the same playbook? Settle the simple part on-chain, keep the complicated metadata off?

Because RWAs and other enterprise tokens point at physical objects, and physical objects exist on their own terms, separate from any ledger. A USDC token is the on-chain dollar. No gap between representation and thing. But a token representing a shipping container is a reference to a box on a truck in Jakarta. Did it arrive? Same box? Contents intact? No chain can know any of that without trusting an oracle, a sensor, or a human being - which is the exact dependency blockchain was supposed to remove.

Consensus cost makes this worse. Validating “Alice sends Bob 50 USDC” across a global validator set is expensive but worth it. Trustless settlement for financial state has high value. Validating “container AB1234 customs status updated to partially inspected, revised ETA July 21” costs the same in consensus overhead. But that data is nested, contextual, partial. You pay the decentralization tax without getting the decentralization benefit.

What this framework misses Link to heading

I’d be overstating if I said the system-of-record lens explains every failure outside finance. It doesn’t. Web3 gaming had a sound structural premise. Blockchain as a system of record for in-game items, simple ownership data model - it could have worked on an architecture level. But most studios shipped tokenomics first and game experience second. Gamers can smell a cash grab. They left. Product failure, not architecture failure.

Web3 social ran into network effects. A decentralized social graph is an interesting technical idea, but my friends are on Instagram. Yours probably are too. Nobody migrates their social life for protocol elegance.

Enterprise pilots hit organizational walls as much as technical ones. I’ve sat in rooms where the proof-of-concept worked without a hitch, and then watched legal sign-off across four partner organizations take longer than building the solution. Multi-party enterprise coordination is brutal regardless of tech stack.

Finance had both the right architecture and product-market fit. Gaming, social, and enterprise were often missing both.

Where this leaves us Link to heading

Blockchain didn’t become the universal trust layer that the 2017 era predicted. What it became is financial plumbing. Good financial plumbing, mind you. Programmable settlement, tokenized ownership, a way to move value with fewer intermediaries than before. And all the complicated parts of finance - risk management, compliance, regulatory reporting - stayed right where they were, in systems built for that job.

A narrower outcome than the original vision? Sure. But a new class of global financial infrastructure processing tens of trillions per year is not a small thing. It’s just specific.

I think we’re still in early stages of understanding where blockchain fits and where it doesn’t. System of record vs verification layer isn’t a perfect framework, and there are edge cases I haven’t covered here. But it gets closer to explaining what happened with blockchain adoption than the “blockchain for everything” narrative, or the “blockchain for nothing” counter-narrative.

We’ll see how it plays out. At least the map is getting more accurate.

PS: This article was written with AI assistance. The core thesis, supporting research, and editorial judgment are mine. It’s 2026 - I’d rather spend my time thinking than typing. Never again!.

PPS: This post was first published as an X article here.